For nearly more than a decade, tokenization has been one of the most talked-about concepts in financial services. From early blockchain pilots, to experimenting with real-world asset trading, to the DeFi boom (Decentralized Finance), the idea has been the same: transform traditional assets such as stocks, bonds, deposits, treasuries, or real estate into digital tokens that can move instantly and trade globally.

Financial institutions have run pilots, and proof of concepts, and published whitepapers, yet tokenized markets have struggled to fully take off. However, that changed recently. Robinhood launched tokenization for over 200 U.S. stocks and ETFs in Europe, proving the concept can work for retail customers. Investors across the EU can now trade tokenized stocks such as Apple, Tesla, or even private equity shares on blockchain rails. While limited in scope, those tokens are the first tangible demonstration of tokenization reshaping access to financial assets. The question is no longer if tokenization will matter, but how will it be scaled.

Tokenization’s transition from an experimental phase into a foundational element of the global financial infrastructure presents opportunities to achieve near-instant settlements, improved liquidity for private markets, and significant operational cost savings. According to an article by PWC,1 tokenization is unlocking revenue in markets that are currently difficult to trade. Tokenization works for liquid assets, such as cash, bonds or cryptocurrency and illiquid assets. Historically illiquid assets, such as private credit and private equity, can also be viable tokenization candidates in the roughly $1.5 trillion private credit market.

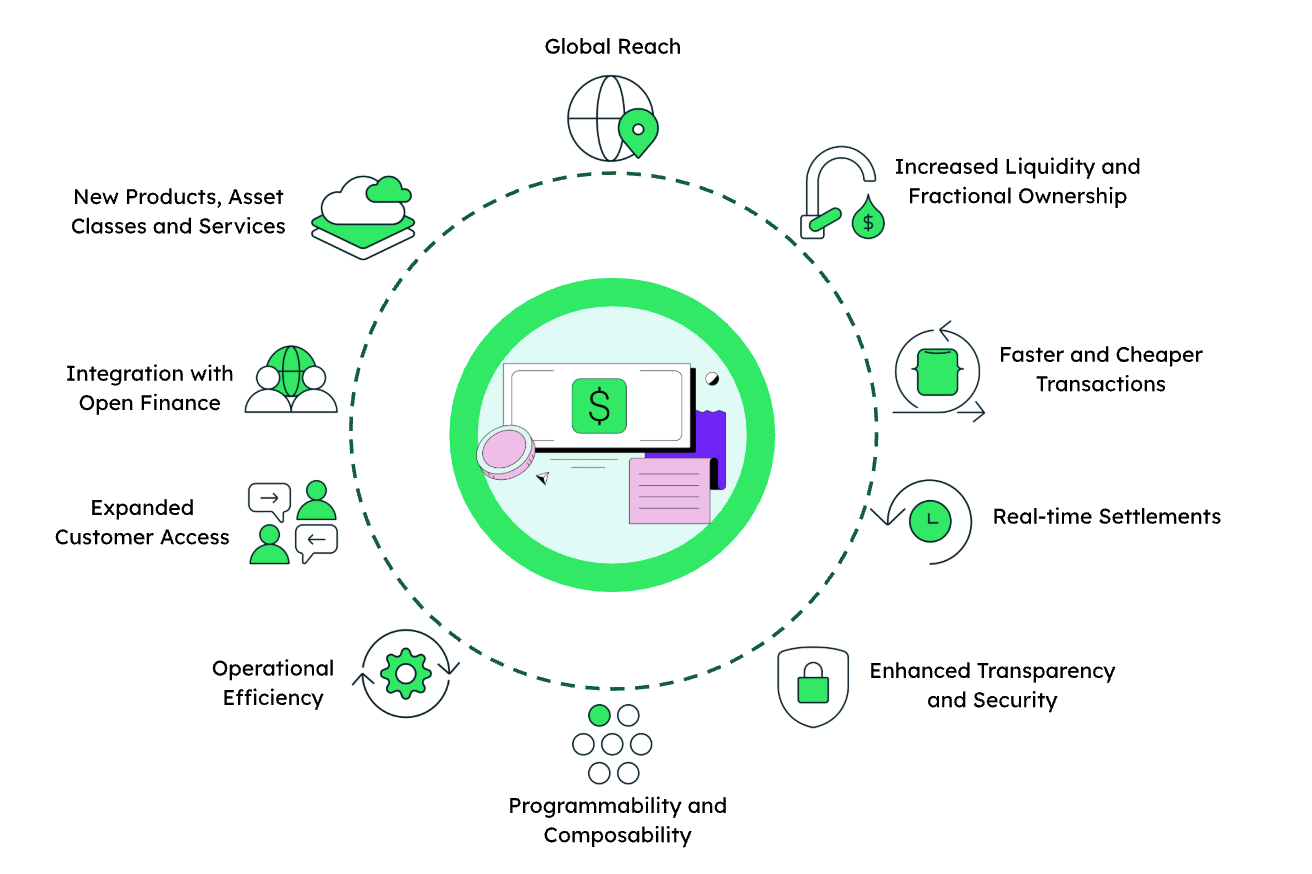

Opportunities and benefits of tokenization

Tokenization offers financial institutions a series of advantages that can modernize operations and enhance customer value. By digitizing assets on blockchains, financial service institutions can achieve:

Increased liquidity and fractional ownership: Assets can be divided into smaller, tradable tokens, allowing retail investors to buy fractions without needing massive capital. This democratizes investment, boosts market depth and creates new revenue streams through increased transaction volumes and expanded market participation.

Faster and cheaper transactions: Blockchain networks enable near-instant settlements, reducing costs associated with intermediaries and paperwork. Trades can occur 24/7, bypassing traditional market hours.

Real-time settlements: Tokenization aligns perfectly with the industry's push toward accelerated settlements. Looking ahead, tokenization enables T+0 or even instant settlements, where trades clear in real-time via blockchain and enhance capital efficiency. Immediate settlement reduces counterparty risk, improves capital efficiency, and enhances market liquidity. For financial institutions, this means lower regulatory capital requirements and improved risk management capabilities.

Enhanced transparency and security: Every transaction is recorded on an immutable ledger, minimizing fraud and enabling real-time audits. Programmable smart contracts automate compliance and reduce errors.

Programmability and composability: Tokens can embed rules (e.g., automatic dividend payouts), allowing assets to interact seamlessly with FSI global ecosystems for new financial products like tokenized loans or derivatives. The programmable approach to regulation could transform how FSI firms manage regulatory requirements and responses.

Operational efficiency: By automating processes through smart contracts, tokenization reduces the need for intermediaries and manual processing. FSI firms can process transactions more efficiently while reducing operational risk, optimizing costs and reducing human error.

Expanded customer access: Financial institutions can offer tokenized products to underserved segments, such as global retail investors, fostering loyalty and attracting deposits through integrated FSI ecosystem services.

Integration with open finance: By tokenizing assets, FSI firms can participate in decentralized economies, collaborating with fintechs for hybrid models that blend traditional banking with blockchain at scale.

New products, asset classes and services: Opportunities in tokenizing real-world assets like art, commodities, or carbon credits could create niche markets, while financial institutions provide custody, trading, and advisory services.

- Global reach: Tokenization taps into borderless networks, enabling FSI firms to serve international clients more effectively, reduce frictions and offer new global products and services where access was not possible before.

Figure 1. Opportunities and benefits of tokenization.

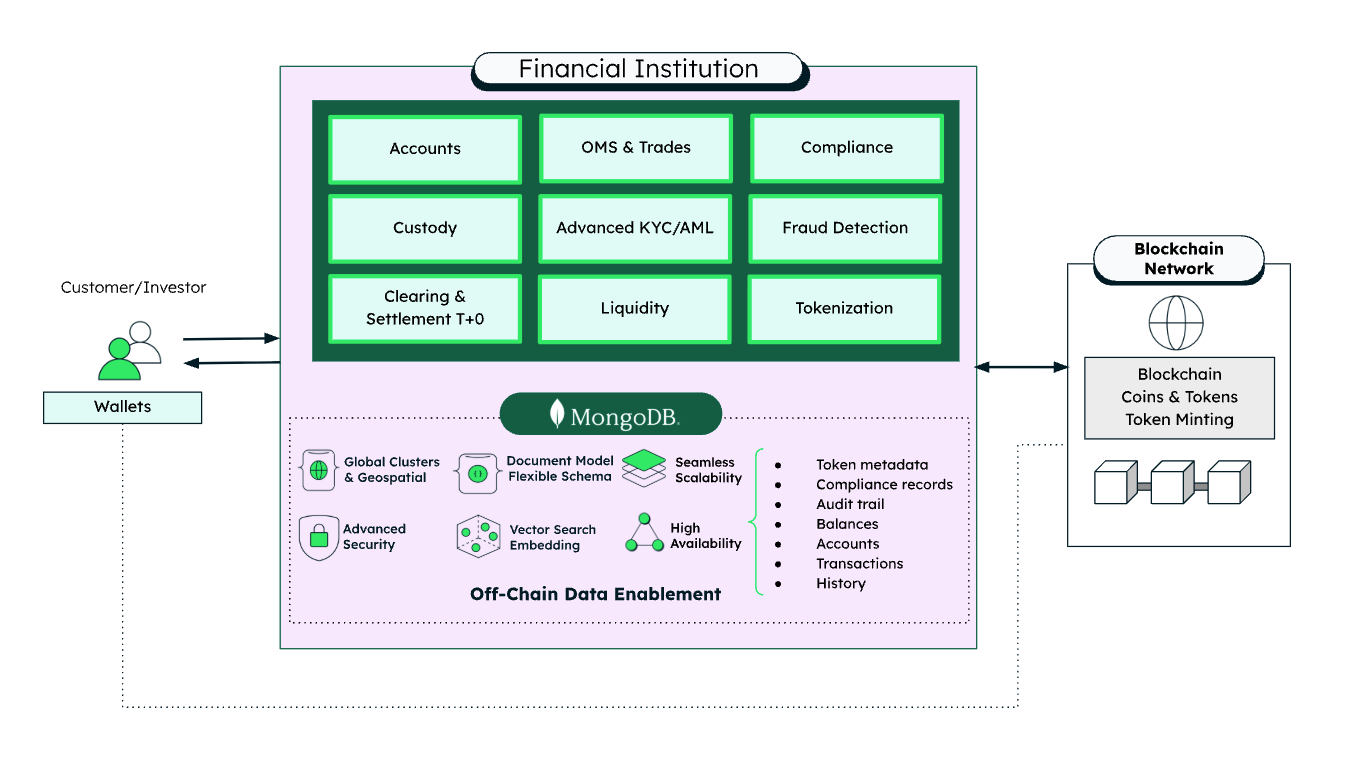

The role of MongoDB in tokenization

Tokenized platforms require a data backbone that is scalable, flexible, auditable, and always-on. That’s where MongoDB plays a critical role. MongoDB acts as an off-chain data enablement layer that supports the operational and compliance processes. Tokens aren’t just balances; they carry rights, lock-up periods, KYC status, settlement histories, and corporate action rules. These data sets can be stored as the metadata associated with tokens and as a registry.

MongoDB acts as a unified off-chain data platform for integrating diverse data sources, enabling seamless interactions and unlocking the following foundational data capabilities:

Flexibility and interoperability in real-time

Tokenization generates diverse data types that traditional relational databases struggle to handle efficiently. MongoDB's flexible data model provides the flexibility needed to store and query blockchain data, smart contract states, and tokenized asset metadata without rigid schema constraints.

The real-time nature of tokenized asset trading requires databases that can handle high-frequency updates and queries. MongoDB's architecture enables the real-time processing requirements essential for T+0 settlement and continuous trading operations.

MongoDB's ability to provide seamless integration with blockchain networks makes it an ideal choice for banks or financial institutions operating across multiple tokenization platforms. MongoDB can serve as a bridge between blockchain networks and traditional banking systems. MongoDB’s ACID transaction support feature can ensure the integrity of high value transactions.

Intelligent insights

To unlock the full potential of this data, financial institutions are increasingly turning to AI for risk assessment, fraud detection, and personalized insights. MongoDB’s AI-ready architecture provides the perfect foundation for an AI workload by handling diverse data types, vector search, embedding/reranking and seamless AI ecosystem integration.

Tokenization generates vast amounts of data that financial institutions must analyze for risk management, compliance, and business intelligence. MongoDB's aggregation framework and analytics and reporting capabilities enable sophisticated analysis of tokenized asset performance, market trends, and regulatory compliance metrics.

Highly scalable and resilient

Financial institutions often require multi-cloud or multi-jurisdiction deployments for regulatory and operational reasons. MongoDB's cloud-agnostic architecture supports these complex deployment requirements while maintaining consistent performance and functionality.

MongoDB provides enterprise-grade security features essential for FSI applications, including field-level encryption, role-based access control, and comprehensive auditing capabilities that support regulatory compliance requirements.

As tokenization scales, financial institutions need databases that can grow with their operations. MongoDB's horizontal scaling capabilities allow firms to handle increasing transaction volumes without performance degradation. MongoDB’s distributed architecture supports tens of thousands of transactions per second, scaling horizontally via sharding as demand grows with no constraints.

MongoDB’s multi-region replications and high availability model through replica sets support 24/7 uptime that is critical for real-time tokenization and T+0 settlement process.

Key challenges facing tokenization

Despite all the promises, tokenization poses certain key challenges for financial institutions to overcome:

Regulatory uncertainty and complexity: Varying global rules on tokens create compliance risks. While regulations are becoming clearer, the compliance landscape remains complex. The challenge is compounded by the global nature of tokenized assets, which may be subject to various regulatory frameworks simultaneously. Firms must navigate advanced AML/KYC requirements and deal with potential liquidity mismatches between tokens and underlying assets.

Cross-jurisdictional operations & compliance: Tokenized assets can cross borders instantly, creating complex compliance scenarios. Financial institutions must develop systems that can automatically apply appropriate regulations based on the asset, investor, and jurisdiction involved.

Interoperability and scalability: Integrating legacy systems with blockchains is complex as most firms operate on decades-old core banking and FSI systems that weren't designed for blockchain integration. Isolated tokenization platforms can create independent solutions that are not able to communicate effectively with existing financial ecosystems or each other.

Cybersecurity and risk management: Cybersecurity threats, like smart contract vulnerabilities, loom large, while uncertain demand for tokenized products could limit scale. Tokenization introduces new security vectors that traditional financial institutions must address. Digital asset security requires different approaches than traditional security, including private key management, smart contract auditing, and protection against blockchain-specific attacks. Custody of tokenized assets and wallet management must meet stringent security standards.

Real-time operations: Maintaining continuity for 24/7 operations represents significant technical and process challenges. Moving to T+0 requires coordination across the entire financial ecosystem. Financial institutions must be able to manage risks in real-time and ensure their operations can handle the scale and volume.

Conclusion

For years, tokenization was a vision without tangible results. The recent development by fintech innovation is a paradigm shift that demonstrates tokenization's commercial viability. It has forced regulators to open new doors and financial institutions to reconsider their tokenization strategies. When Robinhood successfully operationalized tokenization, it validated the technology's potential and created competitive pressure across the industry.

MongoDB provides the foundation to make this a reality, bridging on-chain innovation with the resilient, off-chain data platform that financial institutions require in the digital asset era. MongoDB, as a core data layer, accelerates agility and flexibility that is demanded by the tokenization business landscape. The next five years will likely see exponential growth in tokenized asset volumes, driven by improved regulatory clarity, enhanced technical and data infrastructure, and proven business models. FSI firms that establish strong positions in this emerging market will be well-positioned to use tokenization opportunities as a competitive advantage.

Next Steps

Discover how MongoDB acts as the data layer for new US stablecoin banking systems, offering flexibility, scalability, security, and developer agility in our blog: Accelerating Stablecoin Innovation in US Banking.

Read more about: Powering the Next Generation of Digital Assets Platforms with MongoDB